Money as Protocol, Product, and Asset

A Product Management Approach to Stablecoins

Bitcoin's growth has opened conversations about money to the mainstream.

The number of people who now have some appetite for M2 liquidity, rehypothecation, and even the characteristics of money itself.

However, its original intent as described in the white paper as "peer to peer cash" still seems to be a distant goal (although there's plenty of work being done on it)

What has emerged as the "killer app" (and the question of "What is an app?" does need to be explored) of crypto has been stablecoins - the closest to this vision of "peer to peer cash."

As with any asset, protocol or product in an emerging space, there will be winners or losers; and not all who come first necessarily be able to claim the crown.

This is a way to understand the ecosystem as one would a product in an emerging space, and evaluate the considerations and strategies.

But first, some definitions around "What is a stablecoin?"

What is a stablecoin?

The broad definition adopted is that a stablecoin is a way to preserve a stable unit of account without exposing participants to volatility.

One common way currently is to “peg” the value to the US Dollar.

Bitcoin’s volatility disqualifies it as as a stablecoin; and by extension, stablecoins that have relied upon Bitcoin as a reserve in the past proved unstable (but I don’t think this has to close off this particular product in the future).

However, some would argue that inflation is also a form of volatility; that even if the value is the same today as it was yesterday as it would be tomorrow, if the ability to purchase a given basket of goods changes, then it's also not a stablecoin.

For example, many stablecoins, such as Tether and USDC, are backed 1:1 by the US Dollar; however, the increasing M2 of USD contributes to inflation, and that means purchasing power decreases.

Is the inflation as destructive as that found in, say, Venezuela? No.

But some camps, such as Reserve, would argue that, as a result, dollar-backed stablecoins are not true stablecoins.

Part of this paper is to give a framework for us to evaluate what definitions makes sense (and certainly, it depends upon product issues such as who is the customer, what pain is being solved, and what is the goal for the stable coin itself).

US Dollars - where the real world meets crypto

Despite being a Bitcoin maxi, I recognize the real world and its pace of adoption for products; and the UX or user experience, alone, of Bitcoin vs a digitized US Dollar makes USD-backed stablecoins the winner.

Uncle Sam beats Satoshi in the foreseeable future.

And he may actually prefer to join forces.

Framing the Disruption Vectors

Traditional money depends upon a technology.

Bitcoin has shown that technology innovations, the infrastructure, can enable disruption at the “application layer” — in the case of money, the social construct of money as well as the actual institutions supporting this new belief system.

However, most of the world don’t see money, whether physical dollar bills or numbers on a bank or credit card ledger, as technology.

But it is, and when the underlying technology changes, so does the opportunity for new products to be built, as well as new players for value capture.

These can come from attacking undeserved markets, mechanism design, or exploding new use cases with a better user experience.

In this essay, I’m going to frame the types of disruption that succeeds, and how this has transpired in money to date.

From this, we should begin to think about a strategy for new money systems.

10x Better UX

This seems like a funny point of disruption, and I think it can be very hard, but anything that touches the consumer, UX plays a role in disruption.

The canonical example is Apple.

Whether it was existing sea of computers, phones, portable listening devices….Apple crushed the competition at the upper-end of the markets through superior UX.

For Apple, UX isn’t making things pretty.

They deeply understand the user experience at a psychological level, and then did the hardwork at the backend to make it happen.

One example is iTunes.

At the time, users were unbundling CD albums via peer-to-peer piracy.

Apple understood that the user experience of cherry picking singles was better; and did the hard work of enabling this in their licensing and distribution deals with music studios.

AirBnB entered a market where there were already players in the vacation home rental experience, which is basically what they morphed into once they got rid of the air mattresses.

The inventory, the core product, was essentially the same.

But the UX, which included the imagery, as well as the more complex payment and collections experience, enabled them to disrupt not just the vacation rental platforms, but the entrenched legacy providers as well.

Cost advantages

The UX experience can extend to B2B companies.

Cloudflare was easier to use and set-up compared to the clunky competitors like Akamai, the giant in the space.

However, by reimagining the backend infrastructure of their distributed network, they were able to provide features as disruptive cost.

This meant serving the millions of underserved businesses and attacking the legacy companies from beneath.

Superior costs which allow the underserved, particularly nascent or growing markets, to enter is a compelling form of disruption.

Developer-first Disruption

One of the classic illustrations of how enabling developers to programmatically attack a legacy market is Twilio.

But before I dive into this, building for developers or attracting developers, itself, is not a source of disruption.

Microsoft Windows, Server, and SQL all targeted developers. Microsoft famously focused on building up a compelling base of developers, including it’s .NET framework.

However, Linux disrupted on the OS; Postgres on database side.

Why?

I’ll address that later, but will stick to how developer-first disruption works in attacking industries and companies which have no developer-facing surface area.

Telephony, before Twilio, was a closed "protocol".

Enabling SMS or making phone calls involved alot of "stuff" to do; but the demand was there. The size of telephone companies and all the adjacent businesses around telephony was already large, so demand existed.

In this case, the best possible demand: smaller, more nimble, companies that had a known need for more agile provisioning of telephony services for their businesses or their applications.

By making telephony "a bona fide citizen of the Internet" [^1], Twilio was able to unlock huge value for an untapped market; and as it gained traction, unseat incumbents in larger and larger enterprises.

Because it acted as a "gateway" -- Twilio abstracted the complexity and created a simplified, developer-friendly interface in its own private, centralized protocol -- Twilio captured a meaningful amount of the revenue through usage-based fees: it could charge per-minute, per message fees.

But the key idea, one that seems undervalued, is the massive existing demand.

A similar exercise can be done with the success of AWS.

It's initial products were S3 for storage and EC2 for compute.

AWS made traditional hardware API-enabled for developers; and also shifted to a pay-by-the-drink model.

However, the demand for compute and storage had been built up over the prior decades.

For years, large hardware, software, and consulting vendors educated the business decision-makers around the benefits and necessity of "digital transformation."

Open Sourced and Commodified Infra Wins; Simplifiers and Gateways Capture Value

Let's use another example in terms of who ultimately won in the internet.

The Internet operated as a decentralized network; it's nature is to set as much of its infrastructure free as possible.

So proprietary web servers, like Cold Fusion and BEA, ultimately were eaten by Apache.

Increasingly complex higher-level primitives, like video encoding a streaming by Bright Cove and Flash, were turned into open standards via HTML5.

In terms of browsers, Netscape and Microsoft didn't capture it; Chromium is largely the winner (with Google Chrome capturing the largest share).

The challenge traditionally with open source was value capture.

Linux and Apache, for example, disrupted the operating system and web server businesses for Microsoft and Oracle.

But who benefitted?

I’d argue that Google and Facebook were able to scale out their infrastructure — without paying Microsoft or Oracle licensing fees; and they captured revenue outside of those protocols building their own advertising ecosystem.

They, in turn, managed to disrupt traditional advertising agencies and media conglomerates by providing self-serve (better UX) for advertising at a lower-cost (no large upfront ad spend). They disrupted the media conglomerates who owned distribution (which their massive eyeballs disrupted) and lower COGS (UGC versus studio-grade actors and support staff) which, in itself, was just part of the benefit; really they were able to build custom products across micro-segments of audiences.

What does this mean for money?

Many of the similar concepts can potentially come into play, although the space is still early.

The first question is: what is the old and new in the world of stablecoins and what matters the most for growth and dominance?

Business Models of Money

Stablecoins have a couple of dimensions in which they can play, which includes their strategic strengths and the use cases.

For example, Tether ... what was the value proposition for Tether? USDT-pairs are common in DEX's across assets, which provides a network effect: more trading of those pairs generates more fees, and more fees attracts more liquidity providers, which provides more depth to reduce slippage.

However, it's weakness is a strength of its competitor, USDC -- regulatory oversight.

Specifically AML requirements need greater forms of centralization -- the equivalent of freezing assets. This is an essential component to pass regulation required given USD backing. With the USD goes regulatory oversight.

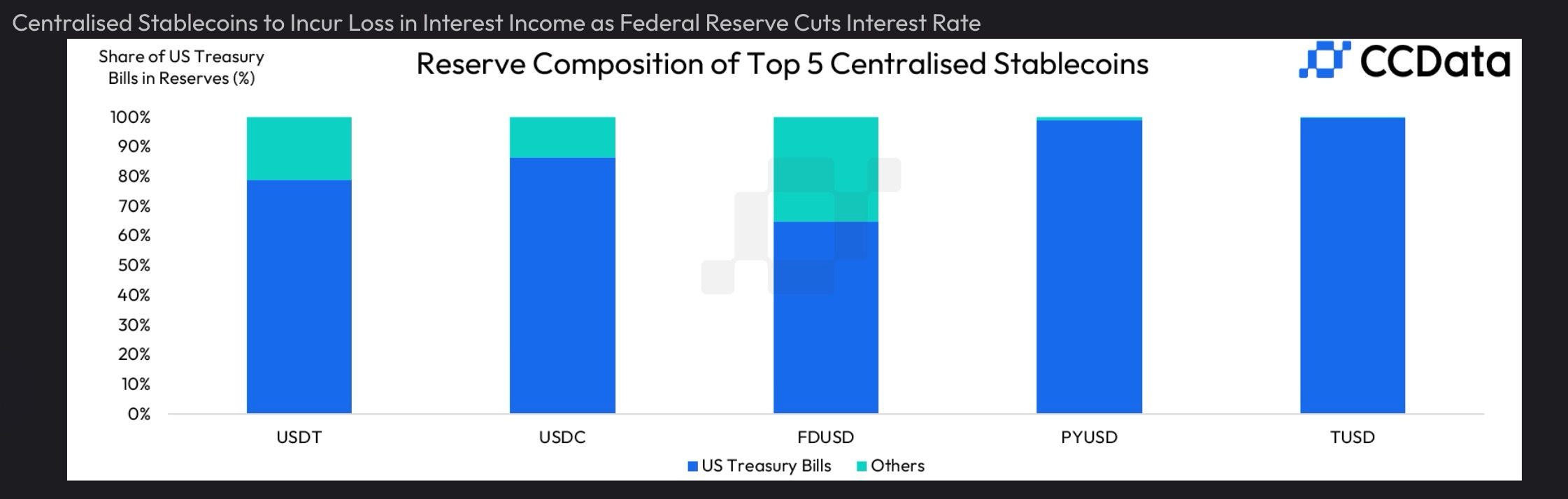

Treasury Bond Interest

Stablecoins like Tether and USDC have a large percentage of their collateral in Treasury bonds. The interest earned is their revenue source.

However, this dependence upon interest exposes them to rate cuts.

> With the top five centralised stablecoins holding combined US Treasury Bills of nearly $125bn, accounting for nearly 80.2% of their reserves, the recent Federal Reserve decision to cut interest rates for the first time since March 2020 is set to result in $625mn in lost annual interest income for each 50bps cut.[^5]

Enabling Fintech Apps

Much of the focus has been to use the blockchain rails for a tokenized representation of the USD; this is a reasonable model that is going to herald the tokenization of real-world assets.

Non Dollar Backed

In an interview on X, Reserve shared that their protocol is enabling any kind of "asset" or R-token that will bundle a set of other assets....these could be any basket of crypto assets, similar to the way an ETF bundles different stocks at different weights to achieve a return.

The thesis is that whoever choses to design such a token will have some insight into the right basket of assets and their weightings to protect against inflation or preserve purchasing power.

But the same idea is behind other deriviates and financial institutions: we saw how seemingly "safe" payment like mortgages could be repackaged into a single entity which could, in turn, be bought, sold, levered and hedged against.

So for the sake of a more narrow definition of "stablecoins", I'll keep that model out for now.

The narrow definition is that the stablecoin is pegged to something that isn't volatile like bitcoin and has low counter-party risks, specifically the ability to "off-ramp" from the token into something that has value.

To me, for global usages, this means, like it or not, the US dollar and short term treasuries.

Governance vs Centralization vs Regulation

One spectrum of concern is the amount of centralization is needed for proper governance and regulation.

For example, while most in the crypto world abhor censorship and are censorship-resistant maxis, are they willing to hold that line if they are advancing a stablecoin?

Are governments willing to give up the ability to apply sanctions — censorship — on the use of funds for bad actors…legitimate bad actors.

This is where the conflict emerge. Pure libertarians seem to believe no government intervention is the best, even if the actors are terrorists.

Governments believe the opposite: oversight and regulation matters, but this has the potential for overreach.

Customers and Use Cases

Who has the problem and who needs to be disrupted to solve it?

For example, **Depositors** would want increased Transparency and perhaps, for those more sophisticated, Governance into how their deposits are used by banks.

In the United States, many aren't too concerned as long as they are below the FDIC insurance limits; but when a bank run occurs and they face cashflow constraints, they do care.

However, do **Banks** and the recipients of the rehypothecated deposits have an incentive?

Into this space Fintech disruptors have entered. Some have created code-based wrappers around traditional banking services and attacking the key issue -- distribution -- by endabling Banking-as-a-Service platforms. Instead of trying to draw depositors and borrowers to their Bank, Fintech apps are able to bring the banking services to their users.

> in prioritizing settlement functions, many stablecoin issuers have deliberately allowed traditional players to maintain control over the money supply. [^2]

Speculators

Hedge funds and traders that need the liquidity or margin drove the initial adoption.

However, stablecoins are finding a break out from this use case:

> If stablecoins were merely utilized as a form of settlement between traders and crypto exchanges, or as a collateral type on these exchanges, as is commonly alleged, you would expect stablecoin settlement volumes, transaction counts, and monthly active addresses to largely correlate with the crypto market cycles. However, the divergence that appeared throughout the cooling off period in crypto exchange volumes in 2022-23 suggests that stablecoins have meaningful usage outside of mere speculative uses. [^3]

Footnotes

[^1]: [Twilio | Union Square Ventures](https://www.usv.com/writing/2010/02/twilio/)

[^2]: [Reconstructing the Monetary Stack | M^0 Research](https://research.m0.org/research/reconstructing-the-monetary-stack)

[^3]: [stablecoins\_the\_emerging\_market\_story\_091224.pdf](https://castleisland.vc/wp-content/uploads/2024/09/stablecoins_the_emerging_market_story_091224.pdf)

[^5]: [CCData](https://ccdata.io/view-report/ckasoeqwpt)